What's inside

Every Section Your Buyer's Compliance Team Looks For

Eight of the seventeen pages, exactly as generated — no retouching.

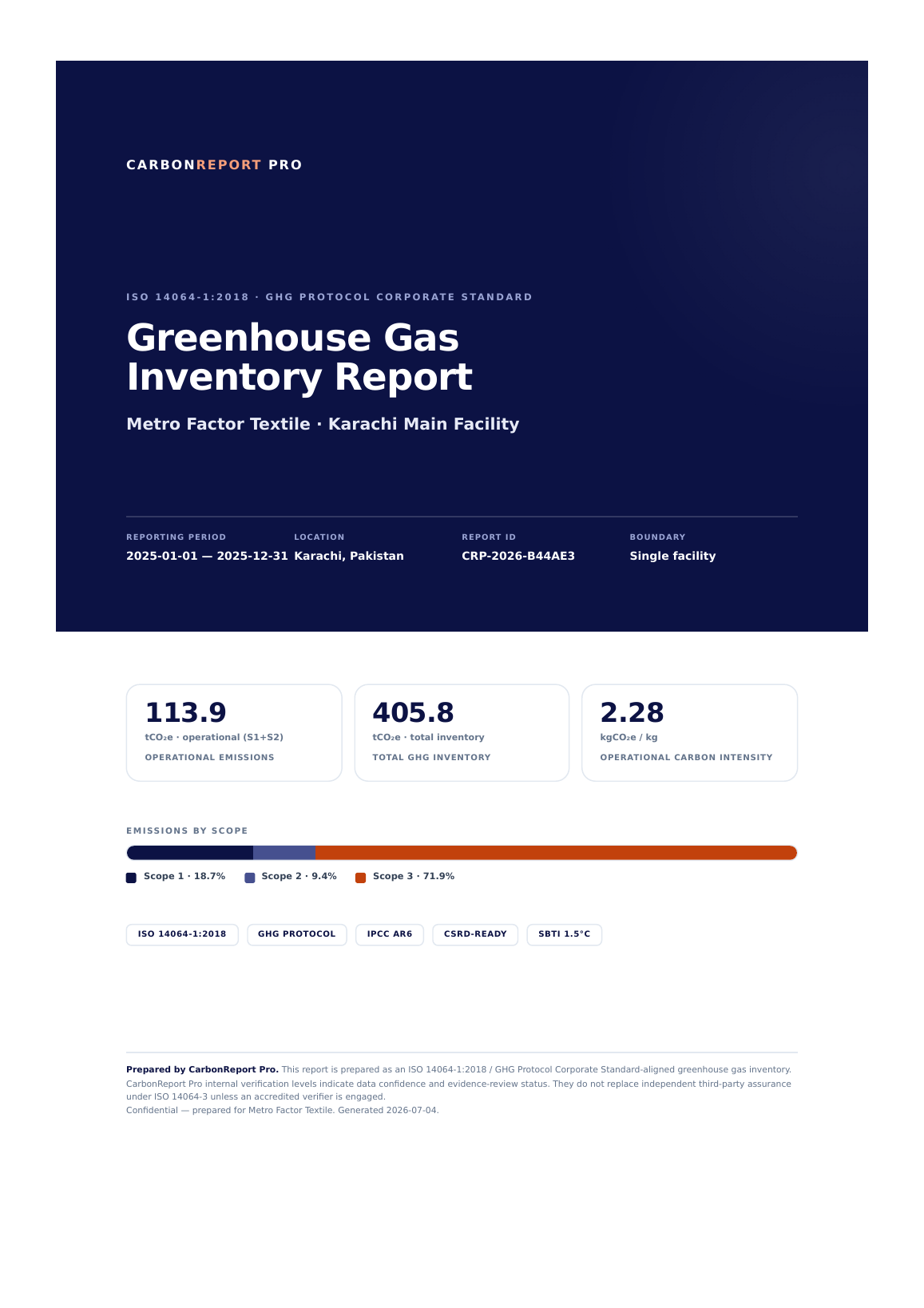

Cover & headline figures

Report ID, boundary, operational vs total split

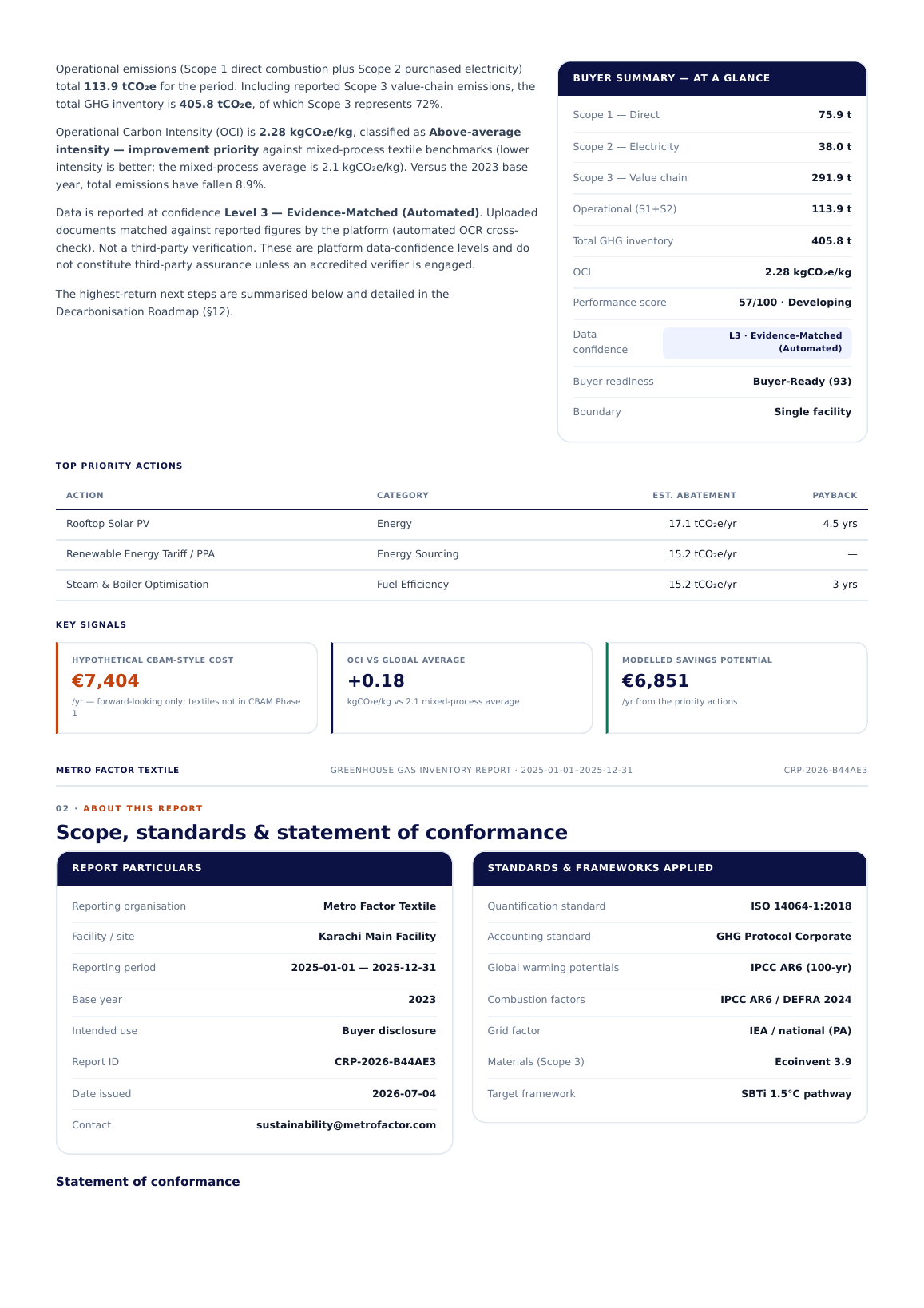

Executive summary

Plain-language findings for decision makers

Scope 2 — electricity

Location-based & market-based, factor sources

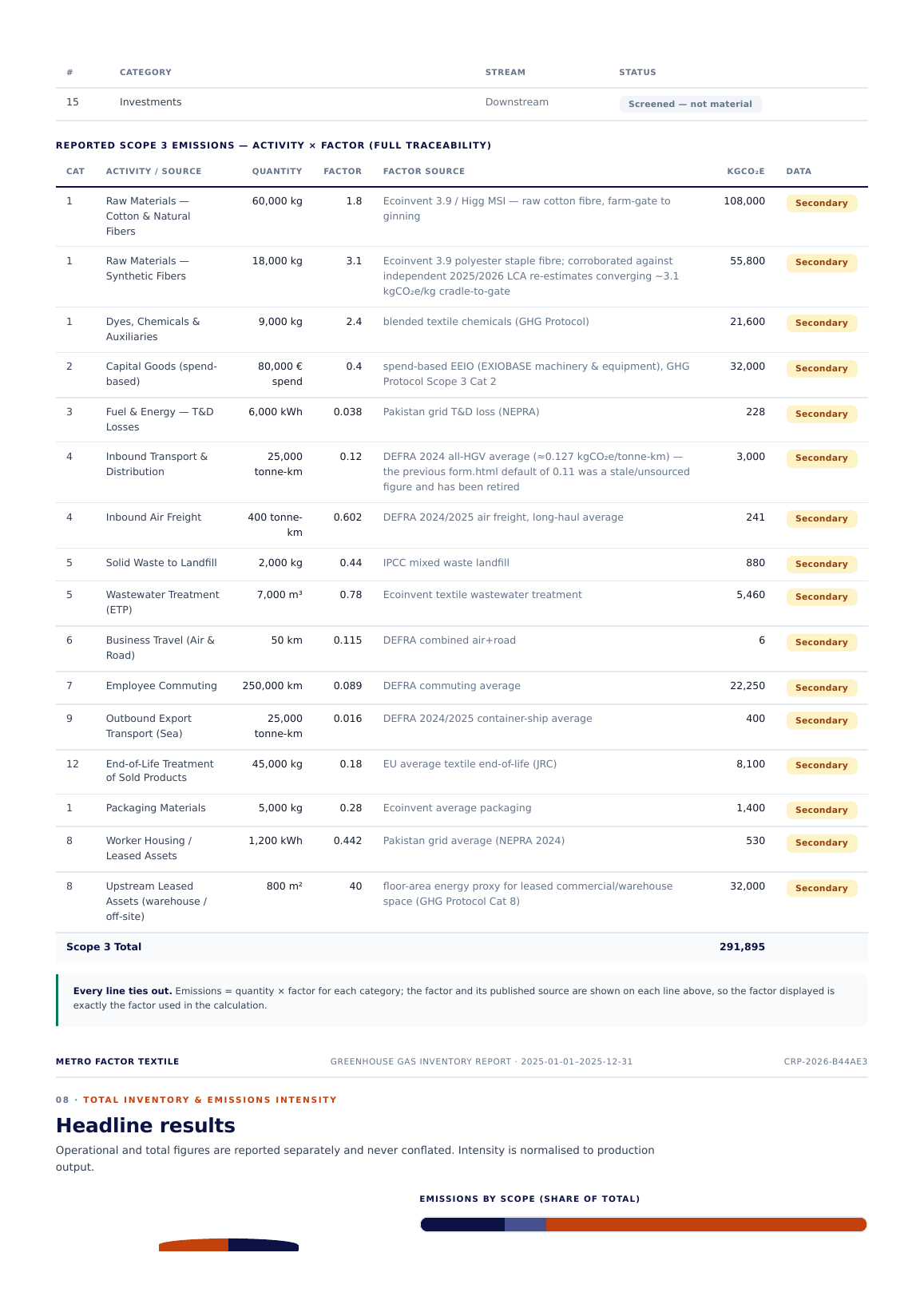

Scope 3 — all 15 categories

Reported, screened and excluded — with reasons

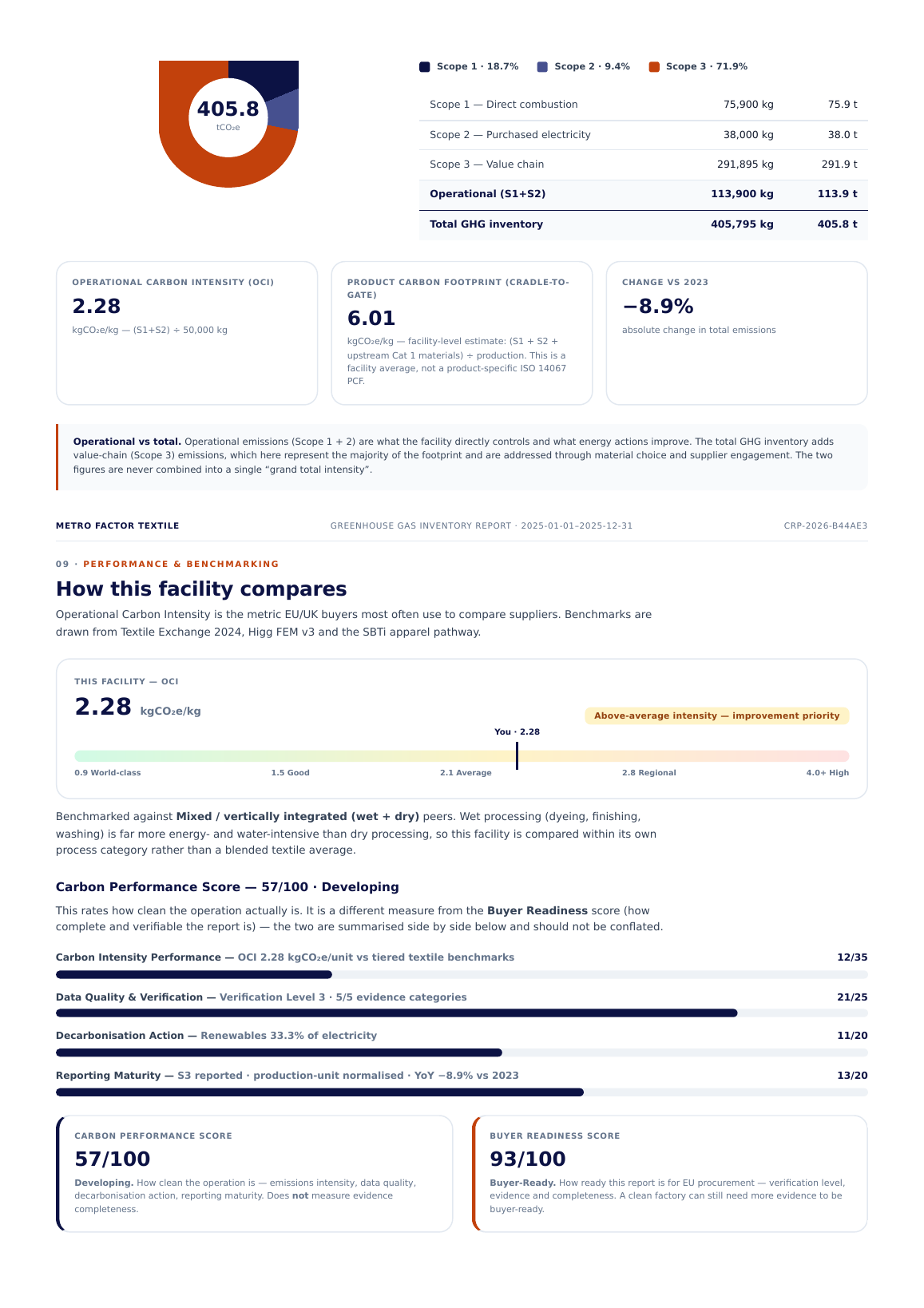

Total inventory & intensity

Donut, scope shares, OCI normalised to output

Benchmarking & carbon cost

Peer comparison + forward-looking CBAM sensitivity

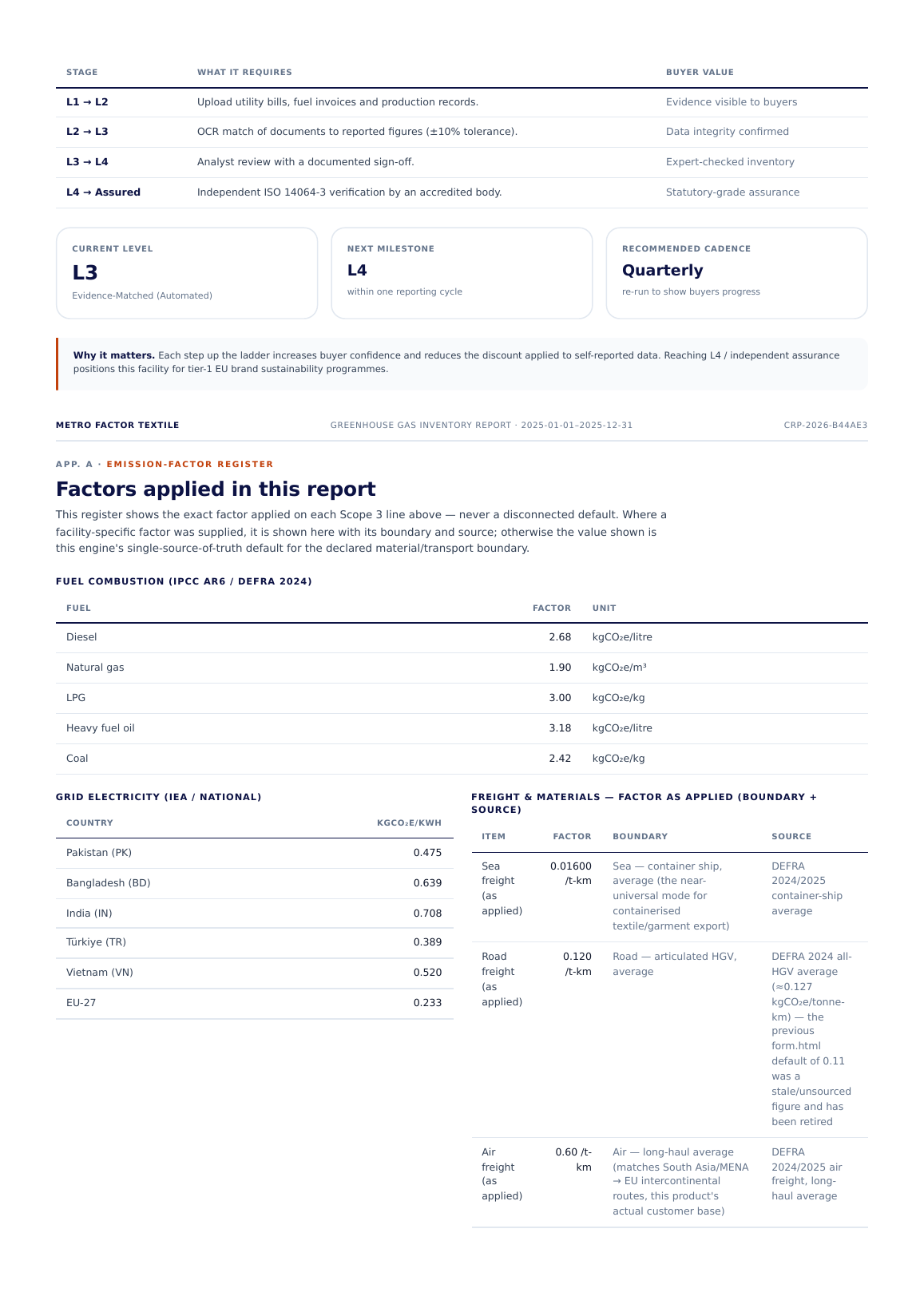

Verification levels

L1–L4 ladder — what each level does and doesn't claim

Emission factor register

Every factor, boundary and source — fully auditable